Options Trading: The Complete Guide to Greeks & Python Tools

Options Trading: The Complete Guide to Greeks & Python Tools

Published 4/2025

MP4 | Video: h264, 1280x720 | Audio: AAC, 44.1 KHz, 2 Ch

Language: English | Duration: 2h 43m | Size: 1 GB

Published 4/2025

MP4 | Video: h264, 1280x720 | Audio: AAC, 44.1 KHz, 2 Ch

Language: English | Duration: 2h 43m | Size: 1 GB

Master options trading by building payoffs, calculating Greeks and IV, and analyzing real strategies using Python

What you'll learn

Calculate Greeks (Delta, Gamma, Theta, Vega) using the Black-Scholes model — fully implemented in Python

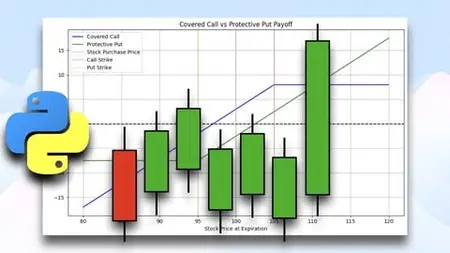

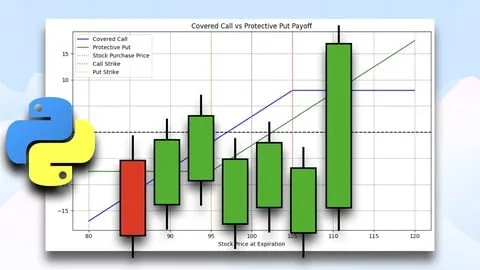

Build and compare real-world options strategies like protective puts, iron condors, and butterflies

Estimate implied volatility using both Newton-Raphson and Brent’s method based on real market option prices

Analyze strategy performance using live option chain data from Binance and Bybit

Understand moneyness, intrinsic vs. extrinsic value, and the role of volatility in pricing and strategy selection

Use Python to simulate, test, and break down payoff profiles across different market conditions

Requirements

Basic understanding of Python (variables, functions, lists, plotting)

No prior options trading experience required — all core concepts are introduced from scratch

Interest in applying Python to real financial markets

Description

This course is designed to turn you into a confident, strategy-driven options trader—without wasting your time on fluff or outdated theory. You’ll learn how to apply options trading in the real world using Python and live market data from day one.We start hands-on: building strategies, calculating Greeks, estimating implied volatility, and simulating payoffs based on actual prices from exchanges like Binance and Bybit. Whether you're a developer, trader, or finance student, this course equips you with the tools to move from theory to execution fast—and with confidence.You'll cover all the fundamentals—calls, puts, payoffs, moneyness—but we don’t stop there. You’ll build full pricing models, calculate Greeks from scratch, and estimate implied volatility using both Brent’s method and Newton-Raphson. You’ll break down and simulate complex strategies like Iron Condors, Vertical Spreads, and Butterflies—and see how they play out using real data from real exchanges.We even explore how options platforms visualize risk and payoffs—giving you a full perspective from code to market execution, and from simulation to strategy validation.By the end of this course, you’ll be able to build, analyze, and understand real options trades—powered by Python, guided by real data, and grounded in strategy that works in today’s markets.

Who this course is for

Finance students and professionals looking to understand and model options in a hands-on, practical way

Python users who want to apply their skills to options pricing, Greeks, and implied volatility

Traders who want to go beyond surface-level options theory and start building real strategies

Anyone who wants to learn how real-world options strategies work — from payoff structure to execution logic — using real market data